Begbies’ interim results show real momentum, with the positive outlook enhanced by two recent acquisitions and an expanded leadership team. The group has confirmed it is on track for both FY26E consensus expectations and its near-term target of £200m revenues.

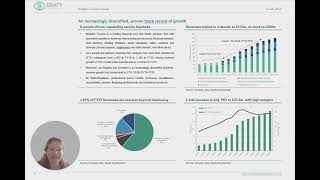

Revenues rose 7% to £82m and Adj. PBT was up 5% to £12.1m. The group’s investment in new senior hires has led to 10% organic growth in the restructuring business, whilst property advisory revenues rose by7%.

This momentum has continued into H226 with an “encouraging flow of new instructions” (and an increased order book of £81.6m), and two delayed corporate finance transactions completed in November.

Surprisingly, Begbies’ shares have fallen over 10% since the summer. With highly profitable organic growth of 5%-6%, and free cashflow to fund both acquisitions and dividends, we see scope for a further rerating.

Our fair value of 150p / share equates to a c.6.5% cal 2026 FCF yield (pre-acquisitions).