Begbies’ H126 revenue and Adj. PBT rose by 7% and 5% respectively, driven by strategic investment in staff, favourable macro-economic conditions, and growth across its breadth of services. The company is confidently on track for FY26E revenue and profit expectations.

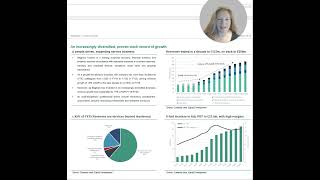

H1 saw further good growth with group revenues +c.7% to c.£82m. Begbies’ core restructuring advisory business led with over 10% organic growth, and Property advisory revenues (30% of group in FY25) rose by 7%.

National insurance increases have cost c.85bps of operating margin, but efficiencies and an underlying improvement in margin have reduced the overall impact to a c.50bps decrease at group level: to a still high 16%.

Management is confident in delivering FY26E expectations (consensus FY26E Adj. PBT of £23.7m-£24.9m) and we make no changes to our overall forecasts. Begbies is well-positioned, generating cashflow to invest in growth and capital returns, whilst the macro-economic environment remains favourable for group activities.

Yet Begbies is trading on only c.6x EV/EBITDA, standing at a material discount to both its long-run average valuation multiples and our unchanged fair value of 150p/ share.